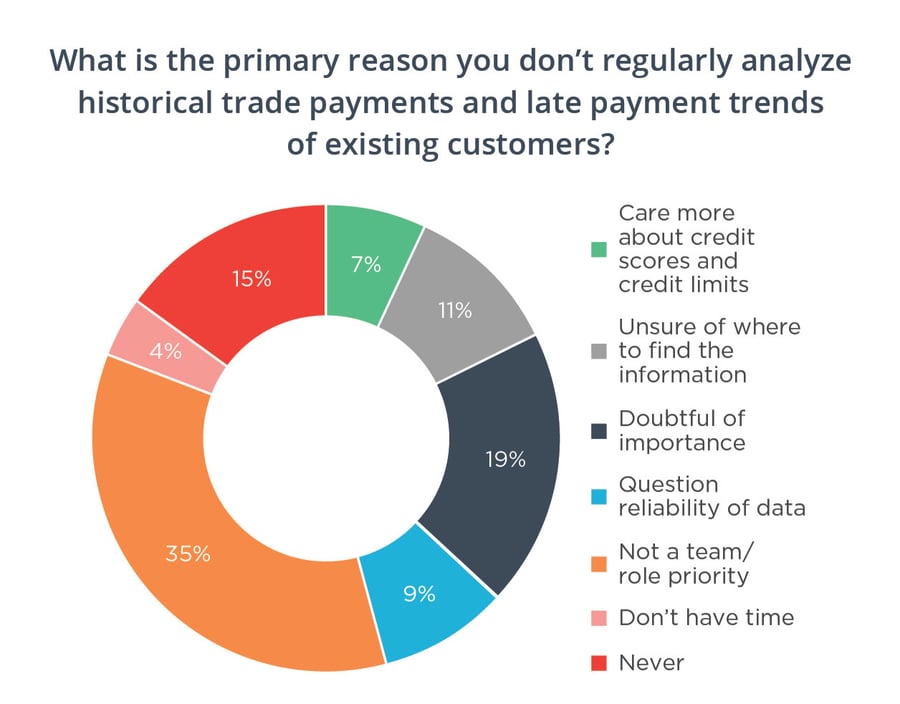

One of the main reasons your customer due diligence might be falling flat is that it simply may not be a priority for your team or within your individual role. That’s what our Cost of Late Payments study found – with 61% of the respondents admitting they don’t always analyze a potential customer’s historical trade payments before signing a contract with them. And when we asked why they don’t do this level of customer due diligence, 17% of the respondents said it wasn’t a team/role priority.

It’s understandable—your sales team is focused on closing deals while your finance team is tied up in strategic financial management, including Accounts Payable, collecting payments, cash flow forecasting and working capital management. With so much to manage every day, we get it; constantly reviewing your customers’ business credit reports and their payment behaviors might fall down your priority list.

But if you’re not analyzing your customers’ trade payment data throughout the customer lifecycle, you could miss out when things change in their financial circumstances. Remember, no customer’s financial health will stay exactly the same from the time you started working with them. They could see expenses rise, while materials and labor costs could rise too. They could lose some customers who account for a high amount of their annual revenue. They may have taken out new business loans or investments from VCs to fund the expansion of the business into new markets or the development of new products. All these factors could come into play – leading to cash flow issues and making it harder for them to pay their suppliers on time.

By making the analysis of your customers’ historical payment behaviors a core part of your customer due diligence, you can spot potential cash flow issues early and make the right decision for your business. That might mean shortening their payment terms, requiring the to pay part or all of their payment up front before delivery of their goods or assessing whether it’s worth working with them at all.

So, if it’s not a current priority for your team or your role, then you can show your business why it should be more of a priority. Show your business – your boss, the head of your finance department, your CFO and the C-suite – how analyzing this type of data can lead to stronger cash flow, less risk and bottom-line growth. Those are things they value. They’ll thank you for it.